Substantial Presence Test: Determine Your U.S. Tax Residency

Have you recently moved to the United States or left after living here for a while—and now you’re unsure if the IRS considers you a U.S. tax resident? The Substantial Presence Test (SPT) is the IRS’s key tool for determining your residency status for tax purposes. Getting this right matters: it determines whether you file as a resident or nonresident, what forms you submit, and how much tax you owe.

At Elmira Tax, our CPAs help international taxpayers and expats confidently navigate these rules. With expert guidance, you won’t have to guess—you’ll know exactly how the IRS sees your residency status and how to prepare your return the right way.

Substantial Presence Test: Determine Your U.S. Tax Residency

Have you recently moved to the United States or left after living here for a while—and now you’re unsure if the IRS considers you a U.S. tax resident? The Substantial Presence Test (SPT) is the IRS’s key tool for determining your residency status for tax purposes. Getting this right matters: it determines whether you file as a resident or nonresident, what forms you submit, and how much tax you owe.

At Elmira Tax, our CPAs help international taxpayers and expats confidently navigate these rules. With expert guidance, you won’t have to guess—you’ll know exactly how the IRS sees your residency status and how to prepare your return the right way.

What Is the Substantial Presence Test & Why It Matters

The Substantial Presence Test helps determine if you’re a U.S. tax resident. Residency impacts how your income is taxed, the forms you must file, and the penalties you could face if you get it wrong.

Definition & IRS Purposes

The Substantial Presence Test is the IRS’s formula-based method for deciding whether a non-U.S. citizen has spent enough time in the country to be treated as a resident for tax purposes. Unlike immigration residency, this test is purely about day count.

The IRS uses the SPT to ensure fairness: someone who effectively lives and works in the U.S. long-term should be subject to the same tax rules as citizens or green card holders. Meeting the test means you may need to report worldwide income—including earnings from foreign sources, rental properties, or overseas bank accounts.

Think of it like a “time clock.” Every day you spend in the U.S. adds up, and when you cross the threshold, the IRS switches your tax status.

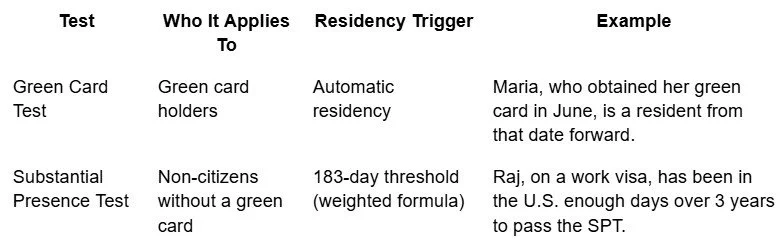

SPT vs. Green Card Test Comparison

There are two main ways the IRS decides residency:

The Green Card Test is about status; the Substantial Presence Test is about presence. If you don’t have a green card, the IRS relies on SPT to decide.

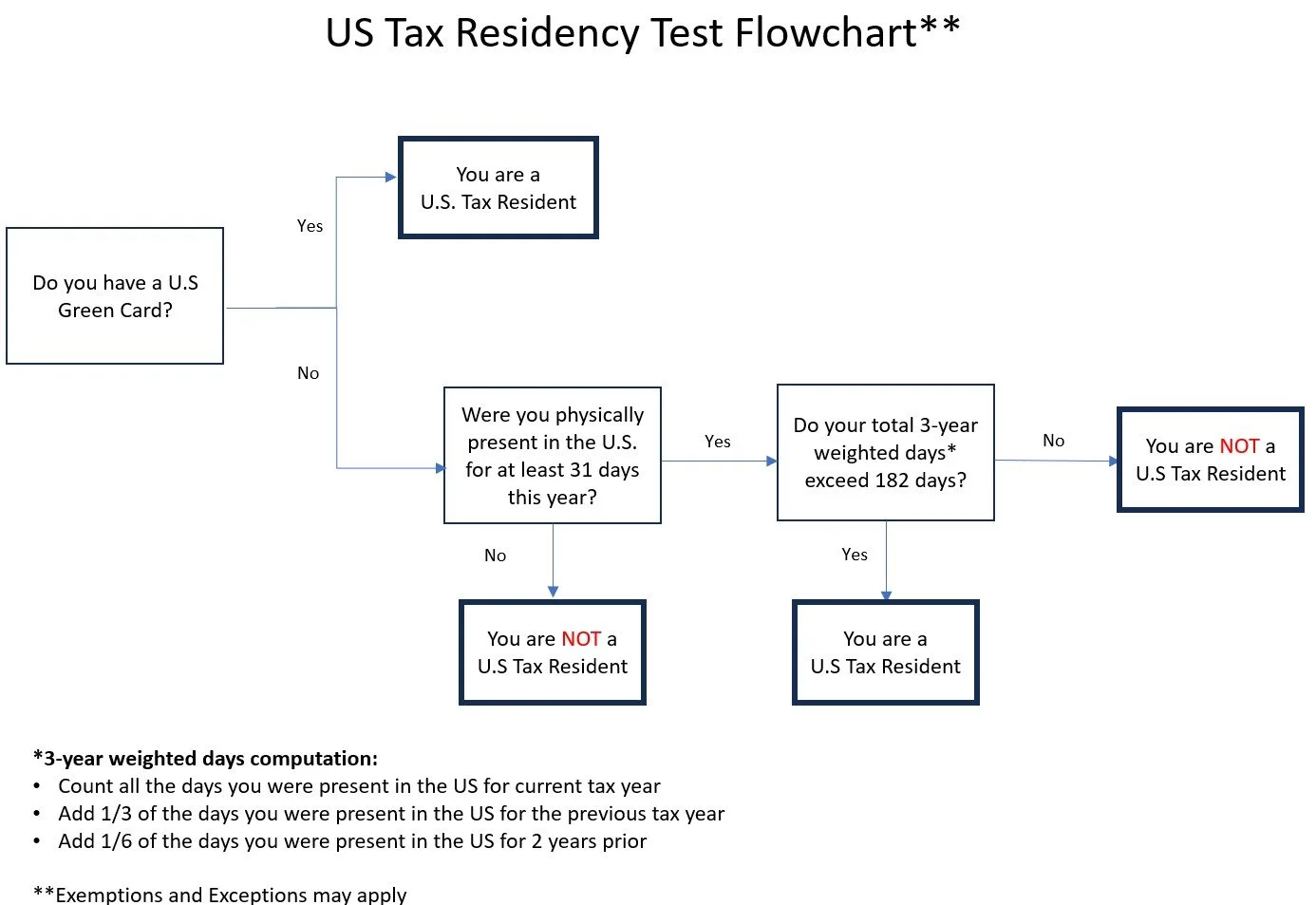

How to Calculate the Substantial Presence Test

The IRS doesn’t just count days in a single year—it uses a rolling three-year formula. Understanding this formula is crucial to knowing whether you qualify as a U.S. resident.

Formula Explained: Current Year, Prior Years Weighting

The formula works like this:

Current tax year: Count all days of presence.

1 year prior: Count 1/3 of days.

2 years prior: Count 1/6 of days.

You meet the Substantial Presence Test if both of the below apply:

You were in the U.S. at least 31 days during the current tax year.

The total weighted days over three years equals 183 or more.

This prevents someone from being considered a U.S. resident based on brief or scattered visits.

Sample Calculations and Embedded Calculator Widget

Example 1: Residency triggered

2024: 120 days → 120

2023: 150 days x ⅓ → 50

2022: 180 days x ⅙ → 30

Total = 200 weighted days → Resident for 2024 (more than 183 days)

Example 2: No residency

2024: 25 days → 25

2023: 90 days x ⅓ → 30

2022: 60 days x ⅙ → 10

Total = 65 weighted days → Nonresident for 2024 (less than 183 days)

Example 3: No residency

2024: 25 days → 25

2023: 365 days x ⅓ → 121

2022: 365 days x ⅙ → 61

Total = 207 weighted days → Nonresident for 2024 (less than 31 days in the current tax year)

Common Exceptions & Exemptions to Exclude Days

Not all days in the U.S. count toward the Substantial Presence Test. The IRS allows exemptions for certain visas and circumstances, which can reduce your total day count.

Exempt Individuals (F-1, J-1, A, G, M, Q Visas)

Some visa holders are considered “exempt” from day counting:

F-1/M student visas: up to 5 calendar years exempt.

J-1 exchange visitors: exempt for 2 out of the last 6 years.

A & G visas: foreign officials/diplomats often fully exempt.

Example: An F-1 student present for four years is still exempt. Only starting in year six do their days begin to count toward SPT.

Medical, Transit, Crew-Member, Commuter Exclusions

Other excluded days include:

Medical condition: unable to leave due to illness.

Transit: in the U.S. for fewer than 24 hours en route elsewhere.

Crew members: days working on ships/aircraft are exempt.

Commuters: daily workers from Canada or Mexico often don’t count.

These carve-outs prevent unintentional residency for people not truly living in the U.S.

Closer Connection Exception & Dual-Status Filing

Even if you meet the Substantial Presence Test, there are exceptions that can help you avoid U.S. residency or split it between years.

When and How to Claim Closer Connection Exception (Form 8840)

If you maintain stronger ties to another country—like a permanent home, family, bank accounts, or business—you may file Form 8840 to claim a closer connection exception.

Example: Sofia lives in Spain, works remotely, and spends 120 days each year in the U.S. for projects. She meets SPT, but her permanent home and family remain in Spain. By filing Form 8840, she avoids U.S. residency.

Dual-Status Resident Election: How It Works and Filing Strategy

If you moved mid-year, you may be classified as dual-status—a resident for part of the year and nonresident for the other. This means filing both Form 1040 and Form 1040-NR in the same year.

Example: Ahmed arrives in the U.S. on August 1 with an H-1B visa. For Jan–July he is a nonresident; for Aug–Dec he is a resident. Proper planning ensures income is taxed fairly.

Tax Filing Implications: Forms, Reporting & Deadlines

Your residency status drives everything about your tax return—from which form you file to whether you must disclose global assets.

Filing as Resident vs Nonresident—1040 vs 1040-NR

Residents (Form 1040): must report worldwide income (U.S. + foreign). They can claim tax credits (e.g., foreign tax credit) to avoid double taxation.

Nonresidents (Form 1040-NR): report only U.S.-sourced income (wages, real estate, etc.). They cannot claim the same deductions as residents.

Residency status changes your tax liability and benefits dramatically.

Additional Forms: 8840, 8843, FBAR, FATCA Disclosure (Worldwide Income Reporting)

Form 8843: for exempt individuals (students, teachers, diplomats).

FBAR (FinCEN 114): required if foreign bank accounts balances exceed $10,000 at any point during the year.

FATCA (Form 8938): foreign asset reporting for residents. Higher filing threshold than FBAR and depends on filing status.

Form 8840: closer connection exception.

Failing to file these can lead to fines up to $10,000 per violation, making professional guidance essential.

Real-World Scenarios & Visa-Specific Examples

Different visas and circumstances affect how SPT applies. These examples highlight common situations.

F-1 Student Case—Under 5-Year Exemption

Ana, an F-1 student who arrived in 2022, is exempt through 2026. Her days don’t count toward SPT until her 6th year. She files Form 8843 annually to claim exemption.

H-1B Worker Case—Residency Triggered

David enters the U.S. on an H-1B visa in January 2025 and stays all year. He easily meets 183 days and must file as a U.S. resident, reporting worldwide income.

Canada/Mexico Commuter Scenario

Luis, a Canadian who commutes to Detroit for work daily, is exempt from counting those days. Despite frequent presence, he avoids U.S. residency under commuter rules.

Visual Guide & Interactive Tools for Clarity

Flowchart: Are You a U.S. Tax Resident

Step-by-Step Checklist ("Calculate → Exclude → Elect → File")

Calculate

Count all the days you were present in the US for current tax year

Add 1/3 of the days you were present in the US for the previous tax year

Add 1/6 of the days you were present in the US for 2 years prior

Exclude

Subtract exempt days (student, teacher, diplomat).

Remove days due to medical, transit, or commuter rules.Elect

Consider claiming closer connection (Form 8840).

Evaluate dual-status residency if you moved mid-year.File

Resident → Form 1040 + possible FBAR/FATCA.

Nonresident → Form 1040-NR + Form 8843 if exempt.

FAQs & Troubleshooting Common Issues

Common questions about the Substantial Presence Test include:

“I Missed Days—What If I Don’t Meet 31 Days?”

You must spend at least 31 days in the current year. Without that, you cannot be a tax resident under SPT—even if your 3-year weighted total exceeds 183.

Tax Treaty Tie-Breaker Conflicts

When both the U.S. and another country claim residency, treaties resolve conflicts. The “tie-breaker” considers permanent home, centre of vital interests, habitual abode, and nationality.

What If I Overstayed Without Knowing?

If you cross the SPT threshold accidentally, you may face unexpected worldwide tax obligations. Filing late or incorrectly can trigger penalties, but working with a CPA ensures corrections are handled properly.

Final Thoughts: Why Work With Elmira Tax

The Substantial Presence Test may seem simple at first glance, but exemptions, exceptions, and filing strategies make it potentially complex. Getting it wrong could mean paying unnecessary tax—or facing penalties for missed reporting.

At Elmira Tax, we specialise in guiding non-citizens, expats, and international professionals through residency rules. Our CPAs help you calculate your SPT status, apply exceptions, and file strategically so you stay compliant and protected.

👉 Book a consultation today with Elmira Tax to confirm your residency status and file your return the right way.